What a brutal six months it’s been for Bumble. The stock has dropped 31.4% and now trades at $3.67, rattling many shareholders. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Bumble, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

Why Is Bumble Not Exciting?

Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons we avoid BMBL and a stock we'd rather own.

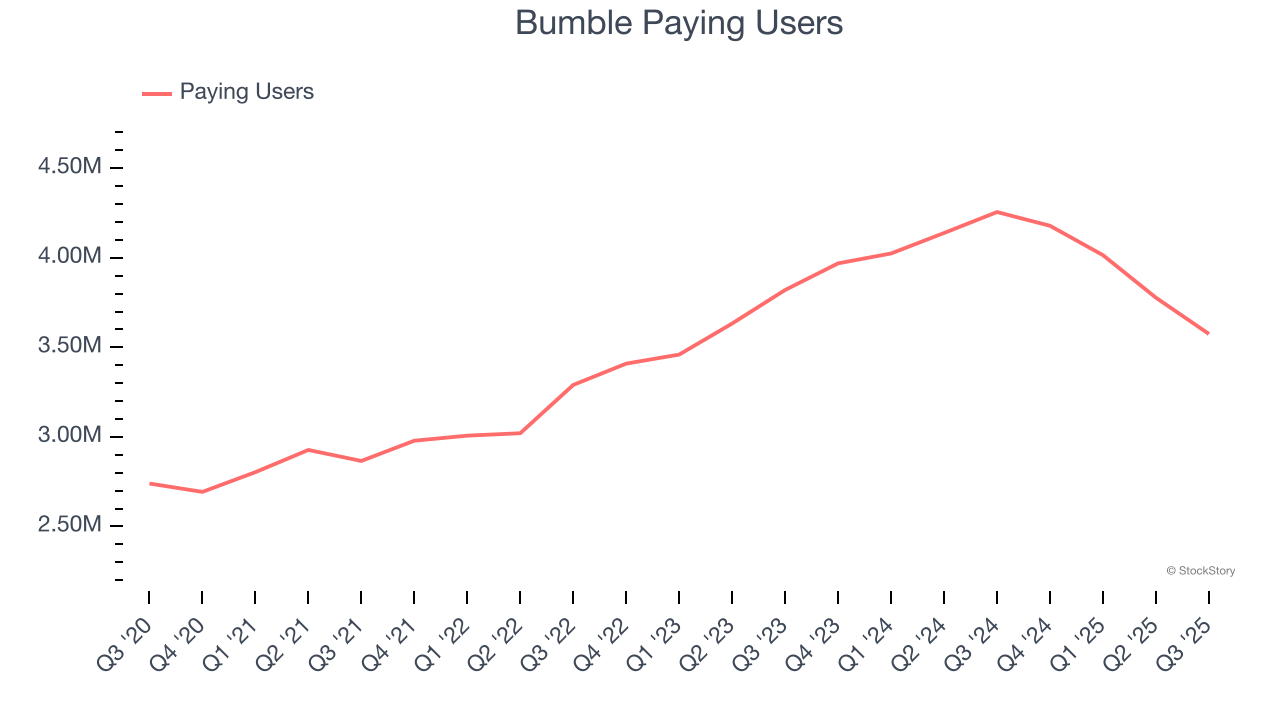

1. Change in Paying Users Points to Soft Demand

As a subscription-based app, Bumble generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Over the last two years, Bumble’s paying users, a key performance metric for the company, increased by 4.8% annually to 3.57 million in the latest quarter. This growth rate lags behind the hottest consumer internet applications. If Bumble wants to accelerate growth, it likely needs to engage users more effectively with its existing offerings or innovate with new products.

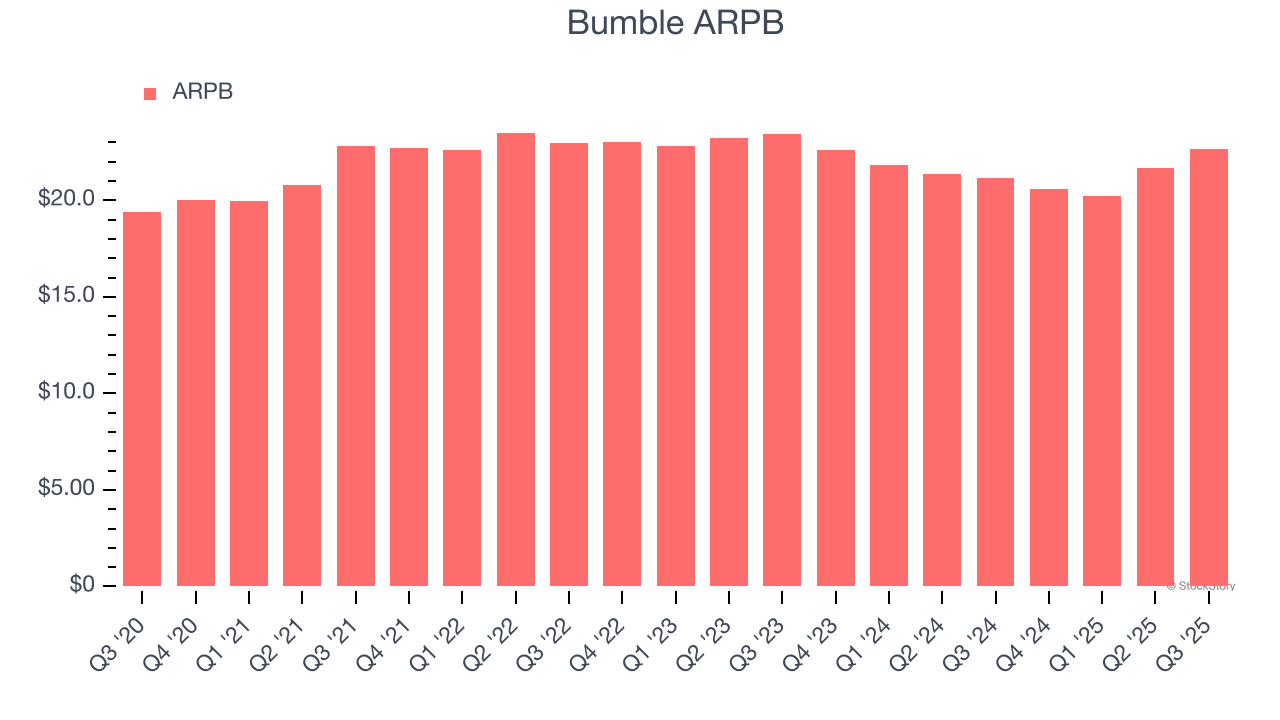

2. Customer Spending Decreases, Engagement Falling?

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much the average buyer spends. ARPB is also a key indicator of how valuable its buyers are (and can be over time).

Bumble’s ARPB fell over the last two years, averaging 3.9% annual declines. This isn’t great when combined with its weaker paying users performance. If Bumble tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether buyer growth would be sustainable.

3. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Bumble’s revenue to drop by 13.7%, a decrease from This projection is underwhelming and suggests its products and services will see some demand headwinds.

Final Judgment

Bumble isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 2.3× forward EV/EBITDA (or $3.67 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at an all-weather company that owns household favorite Taco Bell.

Stocks We Would Buy Instead of Bumble

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.